6 One Way, Half a Dozen the Other

Looking back on our previous post about historical 4th quarter performance, after October it looked like we were staring down a 4th quarter with negative returns. Refreshing everyone’s memory, only about 20% of the time does the market produce negative returns during the 4th quarter of the year. Well, things have changed quite a bit since November 1st, assuming the stock market gains hold through the end of the year. As we write this, the Dow hit a new record high, closing over 37,000 for the first time while the S&P 500 and Nasdaq are within shouting distance of new highs.

After having three consecutive months (August thru October) of negative returns for the first time since the onset of Covid, we received numerous questions and inquiries on whether it was time to make some changes. The last two years - 2022 and 2023 - were quite different from each other in terms of what did well, relatively speaking of course, and what did not.

As 2022 began, the Fed was just beginning to raise interest rates. They would go on to increase the Fed Funds rate by 425 basis points through the year. Dividend stocks significantly outperformed growth stocks in 2022, while 2023 was the exact opposite. As the market moved sideways for the better part of two years, most investors ended up with a similar result whether they were growth focused or dividend focused…regardless of how they were invested..

How they got there was radically different though. The S&P dropped almost -20% in 2022 while the growthier Nasdaq closed down more than -33%. In contrast, the Morningstar Dividend Composite fell only -3.88% in 2022.

The roles reversed in 2023, where the S&P 500 and Nasdaq Composite posted gains of +22.60% and +40.77%, respectively through December 13th while the Morningstar Dividend Composite rose a more modest +9.33% over the same period.

In 2022, dividend investors enjoyed stability within their stock portfolio. Subsequently, one of the reasons for muted returns from dividend paying equities in 2023 was the ability of investors to obtain returns of close to 5% on cash-like investments. We saw a record number of flows into money market funds, cash deposits, etc. Even though those rates remain for now, they will likely be in the rear-view mirror not too far into the future.

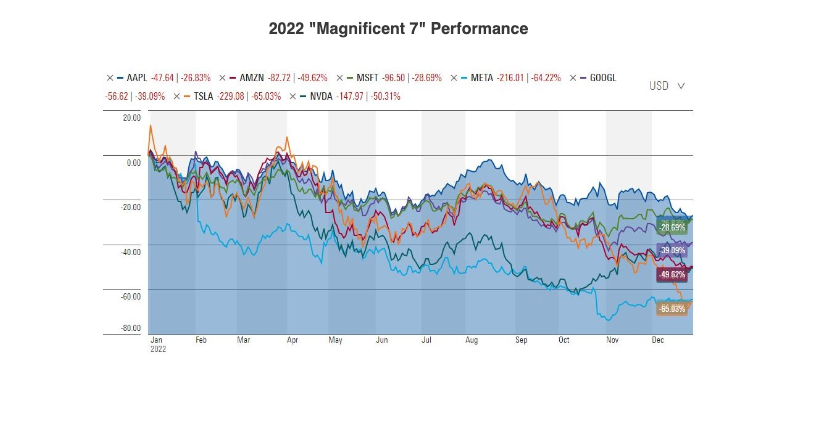

Additionally, higher rates tend to negatively impact numerous sectors such as Real Estate, Utilities and Financial which contain many dividend payers. Not coincidentally, stocks in these sectors moved upward significantly in the last month. For most of 2023, a vast majority of the S&P 500’s gains came from the “Magnificent 7” - Amazon, Apple, Alphabet, Meta, Nvidia, Microsoft, and Tesla. Yet, since November 15th the S&P 500 rallied about 7% while the “Magnificent 7” barely budged, inching up about 1% over the same time period. Is the pendulum swinging? This is yet to be seen.

The past two years tested investors' patience and resolve. Whether it was stomaching a significant downturn with growth stocks in 2022 or seeing dividend payers move sideways for the better part of the last 24 months before their latest surge. Most times, when investors show patience and stick to their plan, they are rewarded.

As always, if you have questions or concerns about your individual situation, please don’t hesitate to contact us.