Officially a "Bear Market"

As the S&P 500 descended and we approached the end of the first half of 2022, it successfully tiptoed around a bear market until last week. For starters, a bear market occurs when a broad market index such as the S&P 500 falls by 20% or more from its most recent high. The index’s peak was on January 3, 2022, and has fallen over 22% year-to-date as of June 17.

To put this into perspective, if the year were to end as of June 17th, this would be the sixth worst annual performance for the S&P 500 dating back to 1926. While the S&P 500 just recently hit bear market status, the tech heavy Nasdaq 100 began its bear market on March 7, 2022, and has declined more than 30% since the beginning of the year.

Rising interest rates, along with a multitude of factors including, but not limited to, inflation, energy issues linked to the Russia-Ukraine War, Covid lockdowns in China, increasing chances of an economic recession and a much less confident U.S. consumer, contributed to the decline in equity prices. While rising interest rates are partially to blame for the slide in equities, they are the primary reason for the simultaneous decline in bond prices. Generally, when interest rates rise, it drives down the value of existing bonds with lower interest rates as investors can purchase a newly issued bond with a higher coupon rate. In most market environments, bonds serve as a counter weight to stocks, not moving much in value and offsetting the risk of owning stocks. This year has been different as bonds have not provided the historical counterbalance to date.

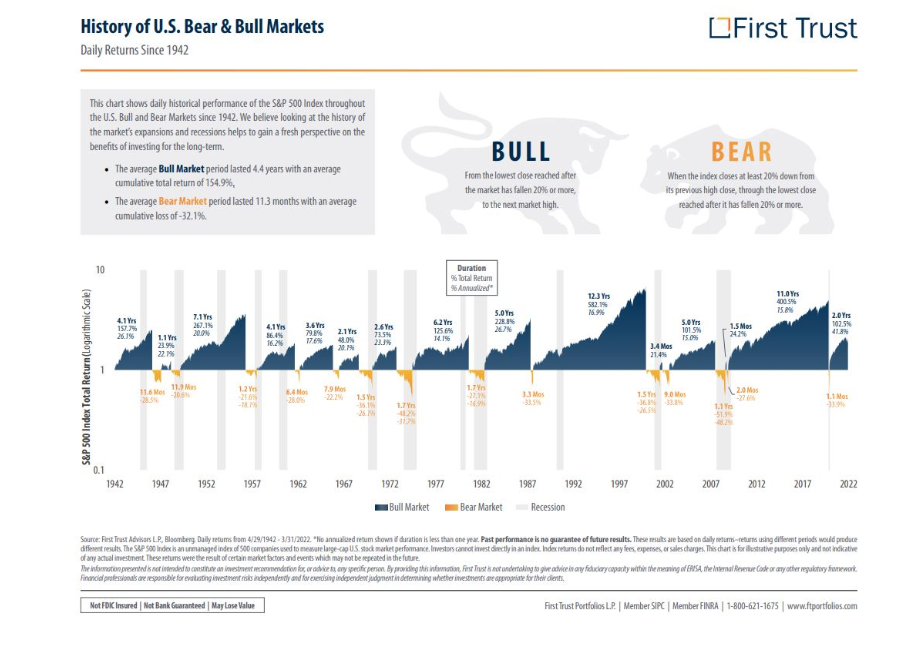

Now that we have hit you with plenty of bad news, let’s move forward on to the positive note. After more than a decade of paltry yields on cash and short-term investments, investors are presented with the opportunity to acquire low-risk US Treasuries and even CDs yielding close to 3% for a one-year maturity. Dating back to 1928, there have been 26 bear markets. After each bear market, a bull market (increase of 20% or more from the low) emerged, all 27 different times. On average, a bear market lasts 289 days. First Trust illustrates bear market / bull market performance and duration below:

Markets in the short-run can be a little bit of a popularity contest but in the long-run, they eventually reward businesses that are profitable, return capital to shareholders and have proven ability to adapt their business to changing economic conditions.

Have we reached the bottom? No one knows for sure, but in times like this, drastically changing your course of action is not a prudent nor recommended investment strategy. Keep your eye on the prize (i.e. long-term goals) and more often than not, investors with patience will be rewarded.

As always, we welcome calls and emails and completely understand if any client has any questions or concerns. Please do not hesitate to reach out to discuss your personal situation and we will continue to provide updates as we move forward.